The 2026 rate environment

Traditional savings accounts remain anchored to the Federal Reserve's benchmark rate. With the federal funds rate holding steady through early 2026, competitive yields are available for risk-averse cash management. Major financial publications report top-tier rates reaching up to 5.00% APY, a significant improvement over the near-zero rates of the previous decade [src-serp-1]. This stability provides a reliable baseline for preserving capital.

However, the spread between traditional bank yields and inflation-adjusted returns is narrowing. Savers seeking to preserve purchasing power are increasingly scrutinizing the real yield after taxes and inflation. This pressure has driven capital toward alternative yield generation methods, particularly in the digital asset space, where protocol-level yields often decouple from central bank policy.

To understand the macro backdrop, it helps to observe the broader interest rate landscape. The chart below tracks the US10Y Treasury yield, a key benchmark for risk-free rates that influences both traditional savings and crypto stablecoin yields.

Traditional savings rates

FDIC-insured savings accounts currently offer a risk-free baseline of approximately 5.00% APY. This rate is several times higher than the national average of roughly 0.40%, providing a stable benchmark for evaluating riskier crypto yields. While traditional banks pay variable rates tied to Federal Reserve policy, these accounts guarantee principal protection through federal insurance.

The following table compares the top three traditional savings accounts as of mid-2026. These institutions offer competitive rates with no monthly fees, making them the standard for low-risk cash management.

| Bank | APY | Min. Deposit | Monthly Fee |

|---|---|---|---|

| Varo Bank | 5.00% | $0 | $0 |

| Ally Bank | 4.50% | $0 | $0 |

| Marcus by Goldman Sachs | 4.35% | $0 | $0 |

Traditional savings accounts require no technical knowledge to operate. Your funds remain accessible via online banking or ATM withdrawals, though federal regulations may limit certain types of withdrawals to six per month. This liquidity and safety make them the preferred parking spot for emergency funds and short-term savings goals.

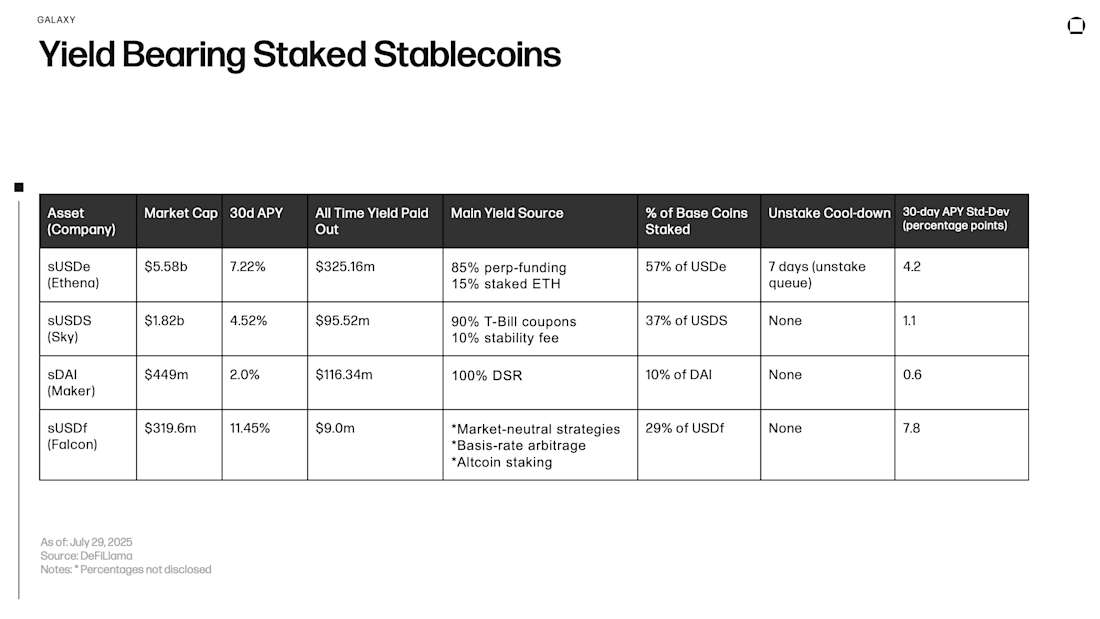

How DeFi Stablecoin Yields Work

DeFi stablecoin yields operate on fundamentally different mechanics than traditional bank interest. While banks lend your deposits to other customers and share a fraction of that profit with you, DeFi protocols generate yield through on-chain lending markets, liquidity provision, and synthetic hedging strategies. These mechanisms allow protocols to capture value directly from market activity rather than relying on a bank's net interest margin.

Protocols like Ethena and Spark illustrate these distinct approaches. Ethena issues sUSDe, a synthetic dollar that generates yield primarily through funding rates in perpetual futures markets. The protocol holds spot stablecoins as collateral while simultaneously taking a short position on the same amount in the futures market. When traders are net-long (paying funding to hold positions), Ethena collects those funding payments, passing a portion of that yield to sUSDe holders. This mechanism can produce high yields during bull markets when funding rates are positive, but it also introduces exposure to smart contract risk and exchange counterparty risk.

Spark Protocol, by contrast, focuses on lending DAI within the MakerDAO ecosystem. Spark acts as a lending platform where users deposit DAI to earn interest from borrowers who take out loans against collateralized assets. The yield here comes from the spread between what borrowers pay and what depositors receive. While this model is more traditional in its lending structure, it still relies on overcollateralized crypto assets rather than fiat deposits, meaning the yield is not backed by government insurance or traditional credit checks.

The key difference lies in the source of the return. Bank interest is derived from the spread between loan rates and deposit rates, capped by regulatory capital requirements. DeFi yields are derived from market inefficiencies, liquidity provision fees, and leveraged hedging strategies. This allows for potentially higher returns but removes the safety net of FDIC insurance. Every dollar in a DeFi protocol is exposed to smart contract vulnerabilities, oracle failures, and market volatility.

Understanding these mechanics is essential for evaluating whether the higher yields justify the additional risks. While traditional savings accounts offer peace of mind with capped returns, DeFi protocols offer higher potential yields with significantly higher risk profiles. Investors must carefully assess their tolerance for smart contract risk and market volatility before allocating capital to these platforms.

Risk and return profile comparison

Choosing between traditional savings and crypto stablecoins in 2026 requires weighing yield potential against structural risk. Traditional savings accounts offer insured, predictable returns, while stablecoin yields provide higher APYs but carry smart contract and regulatory exposure.

Traditional savings

Savings accounts from online banks currently offer APYs around 4% or higher. These accounts are typically FDIC-insured up to $250,000 per depositor, making them the lowest-risk option for preserving capital. The trade-off is lower yield compared to riskier assets.

Stablecoin yields

Stablecoin lending platforms and yield-bearing stablecoins like sDAI or sUSDe often offer APYs ranging from 5% to 10% or more. These yields come from DeFi lending protocols, staking rewards, or treasury yields. However, they lack federal insurance and are subject to smart contract risk, regulatory changes, and potential de-pegs.

Side-by-side comparison

The table below compares key risk and return metrics for both options.

| Feature | Traditional Savings | Stablecoin Yields |

|---|---|---|

| Typical APY | ~4% | 5-10%+ |

| Insurance | FDIC (up to $250k) | None |

| Liquidity | High | High |

| Regulatory Risk | Low | Medium-High |

| Smart Contract Risk | None | Medium |

Live yield tracker

Monitor current stablecoin yields to assess real-time opportunities. Note that these rates fluctuate daily based on market demand.

Key takeaway

Traditional savings offer safety and predictability, while stablecoins offer higher yields with higher risk. Your choice should depend on your risk tolerance and whether you prioritize capital preservation or yield maximization.

Who should choose which option

Your choice between crypto yield and traditional savings depends on two factors: how quickly you might need the money and how much volatility you can stomach. Savings accounts offer FDIC insurance and fixed rates, making them the safer choice for emergency funds or short-term goals. In contrast, stablecoin yields are unsecured and subject to smart contract risk, but they often offer higher returns for capital that can stay idle.

Stick with traditional savings for

If you are saving for a house down payment, a car, or an emergency fund, keep your money in a savings account. The national average for savings is roughly 0.40%, while top online banks like Varo and Synchrony are offering up to 5.00% APY. This insurance protects your principal from market crashes, ensuring you have the exact amount you need when the time comes.

Consider crypto yield for

Crypto yield strategies make sense for surplus capital you do not plan to touch for at least a year. If you are comfortable with the risk of a protocol exploit or a de-pegging event, stablecoins can provide consistent income. This is not a replacement for your safety net; it is a separate bucket for growth-oriented savings that can withstand market swings.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!